What is a PPA? THE Guide to Power Purchase Agreement

Let Pexapark guide you through your power purchase agreement (PPA) journey.

If you are wondering what a PPA is, how it works, or how to optimise it for your renewable project, this guide is for you.

In this article, we will give you an overview of PPAs and their process. At the end of this page, you can download a checklist to use for your PPA negotiation.

What we will cover:

- What is a PPA (Power Purchase Agreement)?

- Why do we use PPAs in renewable energy projects?

- What are PPAs for?

- What are the benefits of a PPA?

- Who needs a PPA?

- What is the PPA process?

- Who writes the initial contract?

- What should you negotiate in your PPA?

You will get:

- Sample PPA contract

- The PPA Prices in Europe (PPA Price Report)

- A PPA Checklist explaining what you should negotiate in your PPA

What is a PPA?

A power purchase agreement (PPA) is a contractual agreement between energy buyers and sellers. They come together and agree to buy and sell an amount of energy which is or will be generated by a renewable asset. PPAs are usually signed for a long-term period between 10-20 years.

Vocabulary tip:

Offtaker is another name for energy buyer. You will also hear an energy seller by other names – such as a generator, an asset owner or an investor.

If you come across any unknown terms, we have you covered. Pexapark’s Glossary of Terms will help you quickly get up to speed at any point while reading our guide.

Pro tip:

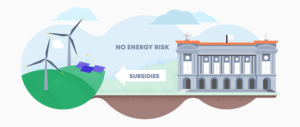

A PPA can cover an existing asset previously under a feed-in tariff (a government subsidy). A PPA can also replace an expired contract.

Note: In a feed-in tariff world, renewable energy investors do not ask how you manage price risk.

What is a Solar PPA?

Thanks to the low cost of solar technology, solar is now one of the cheapest renewables available. That is what makes solar PPAs popular. Generally speaking, a template of a solar PPA is comparable to that of a wind PPA, except for their profile risk. A solar asset has a relatively lesser risk than a wind farm because a solar asset does not produce energy during the night time, for example.

In this article, we speak of PPAs for both solar and wind technology.

Why do we use PPAs in renewable energy projects?

To promote renewable energy, governments initially provide financial incentives for investment such as subsidies (feed-in-tariffs, feed-in-premiums).

With improved technology, renewable assets have become cheaper to build. This leads to a surge in their development.

Consequently, governments begin to move away from subsidy schemes. Either they cannot keep up with the financing or they no longer see the need to provide incentives.

Because the market shift from subsidised projects to open markets has drastically affected renewable investors, they now need to find alternative securities to replace government subsidies.

Feed-in tariff is ending:

Vocabulary tip:

When talking about ‘open markets’, we mean the absence of government involvement, i.e. the absence of subsidies.

What are PPAs for?

For project financing:

Renewables often need a third-party funding source, such as a bank. It is, however, unlikely that a third party will lend without a security.

In the absence of a government subsidy, a wind or solar PPA provides that assurance.

Vocabulary tip:

Third-party lenders can be banks, lenders, credit providers or finance providers.

A typical European 100-megawatt (MW) wind farm can cost between EUR 1-2 million per MW to build. Hence the need for a credit provider – such as a bank – to continually finance a renewable project.

When finance providers require a certain level of confidence in a renewable project, a PPA can provide such confidence. This means a buyer’s commitment to paying a fixed price per megawatt hour (MWh) for a long-term tenor (10-20 years) for the electricity that will be generated by the renewable asset.

From a lender’s perspective, one must also consider counterparty risk. Is this energy seller’s credit profile strong enough to ensure ongoing operation in the next 10-20 years? Lenders call counterparties whom they consider strong enough to finance the cash flows as “bankable”.

COD Project Finance

COD or Commercial Operation Date refers to the date at which the renewable asset 1) becomes fully operational 2) has a grid connection and 3) starts producing energy. Under a PPA contract, COD also indicates a point, from which the obligation of an offtaker to buy the energy begins. In the US, for example, this date typically aligns with the release of a portion of project funding – such as remaining construction costs, potential additional fees, and tax equity. We call this release of final project capitalisation COD Finance or takeout finance.

For hedging:

Power purchase agreements provide a security that the project will bring return on their capital investment upon completion, by reducing the cash flow uncertainty.

PPAs enable the sale of a portion of a project’s future energy generation over the long-term (from 3 and up to 30 years) to an energy buyer. Typically, parties often agree and sign a PPA contract before a project starts.

Pro tip:

Tenors can vary significantly from a market to another.

Investors are like risk managers. They aim to optimise their risk/return ratio. For them, entering into long-term PPA contracts is a way to manage the volatility risk. Prices in power markets are extremely volatile as they can change very frequently (every 5 to 30 minutes).

In such contracts, the offtaker can in turn provide a fixed price for the long-term. This will guarantee a return on investment in the future, with minimum risk regarding expected revenues.

For long-term price predictability:

Electricity prices can fluctuate greatly and frequently. The main characteristic of a power purchase agreement is the agreement to sell X amount of MWh from a renewables project to a buyer of energy at a fixed price.

While this allows a secure future stream of revenue on the seller’s side, the buyer also secures a certain amount of energy at a fixed cost.

Benefits of a PPA

For a renewable asset owner/developer:

A PPA allows renewables projects to increase their level of revenue certainty. Normally, this would not be possible in fluctuating energy markets in absence of a government incentive.

A PPA:

- Enables the financing of their renewable project by lenders

- Reduces risks by efficiently allocating them among the contractual parties

For an energy buyer:

- Assures fixed long-term costs

- Enables a company to (indirectly) fund a renewables project and receive “green attributes”, such as Renewable Energy Certificates

For the lender:

- Offers revenue certainty, as an amount of energy has been sold in advance at an agreed price

- Allow for the claim of their contribution to the renewable industry

Who needs a PPA?

The Energy Buyers

Energy buyers can use PPAs to get their energy from renewable sources. This also enables them to reach their green energy goals.

- Utilities are energy providers such as Axpo (Switzerland), Vattenfall (Sweden) and Holaluz (Spain). They have their own generating assets but also buy additional power to supply their customers. This also enables them to meet potential regulatory obligations set by governments (minimum green energy requirements or targets).

- Corporates are companies with relatively large energy consumption needs across several locations such as: Google, Amazon, and Nike. They buy energy from renewable assets to achieve their ambition of reducing their carbon footprint.

- Industrials are companies that require large amounts of energy for manufacturing, such as a mining company (Alcoa for aluminum production). They would enter into power purchase agreements in order to get certainty on their long-term energy costs.

The Energy Sellers

Energy sellers are the renewable asset owner or developer of renewable assets. We usually call them sellers, although they can fall into the following categories:

- Investment companies that focus on infrastructure

- Independent producers of electricity

- Renewable energy asset managers

- Utilities and energy companies that wish to build their own renewables assets

- Infrastructure funds investing in renewables

How does a Power Purchase Agreement Work?

- Implement, develop or re-finance a project with a PPA

- Determine the structure of the contract

- Create an RFQ and reach out for buyers

- Compare the offers received

- Negotiate the terms

- Sign the PPA contract

- Manage your energy sales and risk throughout the life of your asset

1. How does it start?

The process of a Power Purchase Agreement starts with:

- A renewable project ready to be built. It has a size, location, and a pre-agreed connection to the electricity grid. Or,

- An existing project that needs refinancing

2. Determine the Optimal Hedging Strategy

Form of a PPA

Power Purchase Agreement contracts come in many forms. You may have already heard of physical and virtual PPAs. As a matter of fact, there are other forms too. But for this introduction, we’ll focus on these two.

What is a Physical PPA?

Physical PPAs refer to the purchase of energy at the meter point (the reception point of production). Typically, a utility supplies the energy to its many customers through the existing transmission lines. A Physical PPA customer receives the physical delivery of (or title to) the energy through the grid.

What is a Financial Power Purchase Agreement (Financial PPA)?

A financial PPA, (also called virtual PPA and synthetic PPA) allows a company to buy renewable energy virtually. There is no need to own the title of physical energy. This enables companies to focus on their “green impact”, such as corporates, to receive renewable attributes without owning the asset.

These “green” additionalities allow a credit link between the purchaser and the renewable asset owner. A virtual PPA will not impact the source of energy consumed by the purchasing company.

Read more on the drivers of the increasing popularity of Financial PPAs and frequently asked questions around the structure in our Virtual PPAs: the shift from hassle to bustle blog.

There is a direct correlation between VPPA options becoming more popular and corporates wanting to aggregate demand in multiple countries, or source renewables in locations that it may prove more competitive to do so. Learn more about the concept by reading our Understanding the value of a Cross-border PPA: A guide for corporates guide.

Vocabulary tip:

Renewable attributes are energy credits, renewable energy certificates, etc.

PPAs’ underlying structure

In addition to various contractual forms, PPAs come with different underlying structures and with different forms of hedging that will distribute the diverse energy risks between the buyer and seller. Some of the most common forms include pay-as-produced, annual, or monthly baseload.

In mature PPA markets, availability of Pay-as-Produced (PAP) is decreasing due to cannibalization concerns, and demand for Baseload PPAs is on the rise. Read more on the drivers behind volume preferences in our Baseload PPAs: Essential tips for developers and lenders guide.

3. Sourcing

In order to receive buying offers, the renewable project owner usually goes through a request for proposal or quotation (RFP/RFQ). Interested energy buyers can then make an offer of purchase.

Pro tip:

For large established buyers such as Google, the process can be different. In this case, Google tends to launch private tenders, or auctions, where they invite pre-selected parties to bid against each other in several rounds.

4. Compare PPA offers

Initial offers do not feature details. They contain only core commercial conditions. We call them Term Sheets.

They include, at a minimum, a price, a tenor and a PPA structure. The offers received can vary a lot from one offtaker to another due to different underlying structures, the inclusion of costs (which are not included in others) or different price area basis, among others. Comparing one offer against another can be quite complicated.

At Pexapark, we compare these offers by running thousands of price scenarios based on our proprietary model. This enables us to advise our clients on the optimum structure for their PPA, to maximise their expected revenue and reduce their risk.

5. Negotiation

While sellers and buyers can agree on an approximate price in advance, the details of the contract negotiation can take between 6 to 12 months. There are many important points to agree on.

-> Later in this article, you’ll find our PPA checklist containing 10 commercial points you shouldn’t miss when negotiating your PPA.

Comparing and negotiating are critical parts of the PPA process. Upon signing, a project or an existing project can have better chances for receiving finance or re-finance and construction can start for a specific Commercial Operation Date (COD).

6. Sign the PPA contract

Agree and sign your PPA contract.

7. You have signed your PPA, then what?

Although PPAs guarantee the future purchase and sale of energy at an agreed price today, the sale of an energy asset still needs managing throughout its life. Even though parties can agree and sign a PPA contract for 10 years, the concerned asset may continue on for up to 30 years.

Monitoring the evolution of the market will help you answer these critical questions:

- When is the deadline to re-negotiate a new contract?

- Should I re-negotiate a new contract?

- How much risk am I exposed to now?

- What is the mark-to-market value of my asset?

- If I add an asset to my portfolio, how will it impact my overall risk/revenue exposure?

PPAs are complex financial contracts within a buyer’s financial portfolio. Therefore, we should take their management seriously. Proper value tracking and active management, as well as specific strategies, are crucial for protecting a PPA’s value against volatile energy markets.

This requires a strategy to monitor the asset’s value periodically and perform a mark-to-market valuation (the market value of the asset at a point in time) as prices evolve over time.

It is important to keep track of the exposure to market risks. Such systematic assessment will also identify key contract risks and inform targeted risk mitigation strategies to help lock in a reasonable value at the time of contract signing.

Pro tip:

We often contract PPAs for less than 100% of the asset’s volume. This means that a portion of the energy sales will always be exposed to market risks, even under a PPA contract. Typically, banks require a hedge of 70% of the total production of the asset.

SAMPLE PPA CONTRACT

The buyer is usually the one to create basic offers based on the RFP/RFQ from the energy seller.

Should there be interest on the seller side, the buyer will then provide a more detailed contract. Some more sophisticated buyers such as Google would usually have their own contracts.

In an attempt to standardise PPA contracts across Europe and to reduce transaction costs, the EFET (European Federation of Energy Traders) in collaboration with the RE-Source Platform, have issued a standard Corporate Purchase Agreement (CPPA).

Check out the Sample PPA contract from EFET.

PPA negotiation

You are in the midst of a PPA negotiation….but have you thought of everything?

We got your back and created a PPA checklist to ensure you are covered!

Here are the 10 commercial key points you shouldn’t miss if you want to successfully close your next PPA.

(You’ll find a downloadable checklist at the end of the article.)

- Commercial structure

The type of PPA structure you choose (pay-as-produced, annual baseload, etc.) will impact how the energy risks are distributed among the parties. For example, for the volume risk, in a pay-as-produced structure (a fixed price is paid for any volume produced), the buyer will carry a portion of the volume risk, but the seller is responsible for over – or underperformance.

Whereas in a monthly baseload structure, (a contract that buys a constant volume of energy every hour of each month), the volume risk will be carried by the seller as the volumes are to be guaranteed on a monthly basis.

- Understand Energy Risks

Knowing how much each energy risks you are carrying is essential for negotiating a PPA. This is key to successful contract negotiation.

We recommend you to go over the following 5 key energy risks:

Price Risk:

This risk is the probability that there is an adverse movement in the market price. It is unavoidable but can be mitigated. We take a future position of approximately the same size but in the opposite price direction in an exchange.

Liquidity Risk:

A market is called liquid – if buyer and seller can conclude large volume transactions quickly, without impacting the market price. Depending on the structure of the PPA, its cost or risk can be reduced.

One can achieve this, for example, by getting a validity period (which comes at a cost) or agreeing on a price formula indexed on closing prices. The buyer and seller could agree to fix the PPA price closure referenced on publicly available prices such as forward prices observed on an exchange.

Volume Risk:

The annual energy production of a renewable asset is an estimate. Its likelihood is typically calculated and assessed on the basis of long-term meteorological data.

If a renewable asset is hedging a fixed volume at a fixed price, there is a risk that certain amounts of volume are not produced and need to be procured. If this is the case, the producer may have to purchase the missing volume at market prices that may be worse than the original fixed price. Optimising the volume risk is crucial.

You can make use of insurance guarantees or use certain PPA structures to reduce this risk.

Pro tip: It is important to note, however, that there is always a portion of the volume risk carried by the project owner. What if the plant is not producing any energy? Even under a pay-as-produced structure (when a fixed price is paid for the energy produced), there is a form of volume risk due to potential non-production.

Profile Risk:

Profile risk arises from the fluctuating nature of renewable energy (for example, there is no solar energy produced at night). In markets with high renewable energy penetration, times of high production can mean a significant decrease in power price, that is, revenue.

This will depend of course on the location of the plant and type (solar or wind). You can mitigate this risk by choosing certain PPA structures.

Balancing Risk:

This refers to the difference between what was scheduled (usually a day ahead) and actual production (the imbalance cost). This risk can be reduced by fixing the imbalance cost through an agreement or using intraday trading, if available.

- Duration

Below are some of the most important questions to consider regarding the duration of your contract:

- Do you know for how long the fixed price is set for?

- Do you have to renegotiate the price before the end of your PPA contract?

- How is the start date of your PPA contract defined?

- Will the contract start upon COD (Commercial Operation Day)?

- If production does not happen, is there a grace period? If yes, how long is it and will it come at a cost?

- Price Fixing

Sometimes closing a deal can take months… (from negotiating a PPA contract to closing it). Within these months, market prices can change, i.e. liquidity in the market can change and this could impact the price rather significantly.

In order to mitigate significant price swings in your PPA negotiation, a reference price can be defined. Ideally, you would want daily updated PPA prices… Oh, but wait, we do provide that! Check out PexaQuote, our PPA price software!

- Credit risk (on both seller and buyer sides)

The credit risk refers to the risk that the buyer will not be able to meet its contractual payment obligations agreed into the PPA contract. Know who your direct counterparty is and follow their company’s credit development.

Protections can be put in place, such as advanced payments, margining requirements, increased frequency of payments and a Material Adverse Clause (MAC). The same applies to the seller, e.g. what if the project runs out of money before COD? A guarantee needs to be in place.

- Settlement

Is this a physical or financial PPA? Financial PPAs are hyped in the US but have proven to be unpopular in Europe.

There are two key differences in these PPAs contracts:

Accounting:

A financial PPA is considered a financial derivative and falls under specific accounting requirements set by the IFRS (International Financial Reporting Standards). This is relatively complex accounting which requires mark-to-market valuing.

Physical PPAs, on the other hand, only account for the realised sale, which means a relatively simpler accounting structure.

Credit:

For a financial PPA, the contracted volume will be traded on the market through a TSO and will comply with the credit requirement of the TSO.

For a Physical PPA, the credit requirement will come from the buyer and often at higher credit requirements.

Negative pricing is an increasing issue with renewables. It is thus critical to understand the market in which one is operating and to know how these negative prices are treated. There may be clauses in the contract that forces the asset to stop producing during prolonged negative prices. This is an important and often overlooked item in a PPA contract.

- Underlying contract

Do you have an underlying master agreement contract in place based on the EFET (European Federation of Energy Traders) or an ISDA (International Swaps and Derivatives Association)? If yes, a term sheet usually suffices because the underlying contract has already been negotiated between the respective parties.

If this is not the case, we may want to consider a long-form contract where all the terms of the agreement are defined.

- Changes in law and regulations

What happens if there is a change in the law that materially affects the obligations of one or both parties in the agreement? What if there is a change in the law affecting taxes? This can affect the balance of revenues or risk between the parties.

It is important to know how these changes will be handled in your PPA.

- Performance guarantees

Guaranteed availability is a percentage of the volume that is guaranteed in the contract. Know how under-performance will be contractually treated.

A performance guarantee refers to the case where the production at COD does not meet the contractually agreed-upon expected production. Consider how this settlement will be addressed between both parties. In which case will the seller have to compensate the offtaker?

- Termination

You should know what will trigger an early termination of your PPA contracts, such as a default or COD not occurring before a specific time, and the cost associated with it.

There is a reporting obligation under REMIT (Regulation on Wholesale Energy Market Integrity and Transparency). Under REMIT, wholesale energy market participants are required to report to the ACER (European Agency for the Cooperation of Energy Regulators) on the details of transactions and orders in relation to wholesale energy products (price, quantity, dates, etc.). It is important to note who will take care of obligatory reporting and at what cost.

Pro tip: EMIR (European Market Infrastructure Regulation) is a body that regulates over-the-counter derivatives for financial PPAs.

Conclusion

A PPA is a contractual agreement to purchase an amount of energy at an agreed price, for a certain time, in advance of producing the energy.

PPAs are now common in renewable energy businesses due to the decline of government subsidies. Without subsidies, there is a lack of financial security for lending institutions, such as banks, to invest in a renewables project. As a result, lenders require a new way to secure their investment. A PPA can prove that the concerned renewable asset has already found a long-term buyer at a fixed price.

PPA contracts thus enable renewable investment by providing revenue certainty to investors and lenders in unsubsidised markets.

However, PPAs are complex in their structure and pricing. Overlooking or inadequately negotiating a contractual clause can impact the overall revenue of a PPA project. This necessitates a thorough understanding of energy risks, valuation, and negotiation issues.

Our Pexapark Team takes the weight off renewable investors’ shoulders by guiding them through their renewable projects. We make sure they maximise their revenues.

Get in touch with us today and see how we could help you make the best of your PPA.

Giveaways

PPA Prices:

Due to a general lack of transparency in the PPA market, PPA prices in Europe are not readily available. In fact, the process to get them is cumbersome. You would normally need to contact potential buyers, outline your project, sign NDAs (Non-Disclosure Agreements) and maybe get a price range.

To contribute to a more transparent PPA market, Pexapark provides PPA Prices across Europe for free. Drawing from over 15 years of origination experience, we understand energy buyers and how to calculate fair values of PPAs. We urge you to check it out.

Vocabulary tip: NDAs (Non-Disclosure Agreements) are necessary legal documents to ensure that the information shared between the parties stays confidential.

Origination: The process of originating deals into the trading desk of the company. Providing services and products to solve clients’ energy needs or problems.

EFET Template:

The EFET (European Federation of Energy Traders) published a standard Corporate Power Purchase Agreement in cooperation with RE-Source Platform. In view of standardisation, industry stakeholders have widely circulated and reviewed this CPPA.

Pro tip:

The European Federation of Energy Traders is an association advocating policies and regulations in electricity and gas trading in Europe. It was established in 1999 to support the liberalisation of electricity and gas markets in Europe.

RE-Source Platform:

The RE-Source Platform is a European alliance of stakeholders representing clean energy buyers and suppliers for corporate renewable energy sourcing.

This platform pools resources and coordinates activities to promote a better framework for corporate renewable energy sourcing at the EU and national levels. For more information, visit http://resource-platform.eu/.

PPA checklist: 10 commercial key points you can’t miss in negotiation

Fill in the form to download the PPA checklist